A recent decision by the Central Tax Board demonstrates that the legal form should be respected when determining the tax treatment of carried interest income received from a private equity fund structure.

Background: The Tax Administration’s View

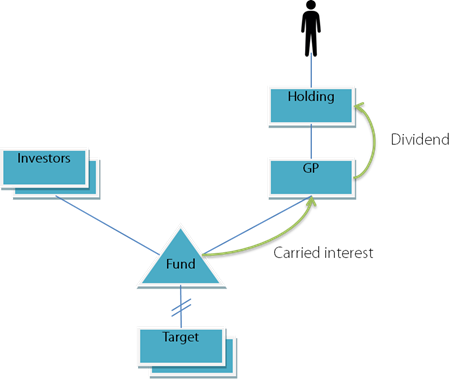

Carried interest is a share of the profits of an investment paid to the fund manager in excess of the amount that the manager contributes to the partnership.

In a two-year project concerning the tax treatment of carried interest compensation and related arrangements, the Tax Administration concluded that carried interest should always be viewed as earned income. The Tax Administration based its view on the following arguments:

- carried interest should be viewed as a form of compensation for the fund’s management;

- carried interest compensation resembles an incentive system based on employment; and

- carried interest does not include the essential characteristics of capital income, such as real risk of loss of capital.

The Central Tax Board Ruling

The Central Tax Board (fi: Keskusverolautakunta) recently examined a Finnish private equity firm’s advance ruling request regarding carried interest. The request concerned the tax treatment of carried interest income paid to the general partner of the fund, from which the profits would be further distributed to its shareholders (see graphic below).

The applicant highlighted, inter alia, that:

- the manager’s carried interest incentive is done at the request of the investors, and the payments are at arm’s length;

- the carried interest payments are made separately from salary and bonuses, and are only to a minor extent dependent on the fund manager’s work contribution; and

- the fund manager’s and their holding companies have a real risk of loss of capital.

In it’s ruling of 11 November 2016 the Central Tax Board confirmed the well-established tax treatment of carried interest income and resolved that the carried interest is to be taxed in accordance with the its legal form, which means that:

- the carried interest received by the GP from the fund is to be taxed as the GP’s taxable income in accordance with Section 16 of the Income Tax Act; and

- the pro rata dividend distribution from the GP to its shareholders should be taxed as dividend income.

We note that the decision is not yet legally binding.